If you live in Cranston or Western Cranston (02921), you may have had a knock on your door after a storm.

A friendly roofer offers to replace your roof and whispers the magic words:

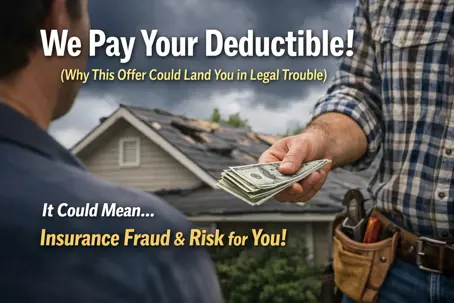

“Do not worry about the $1,000 deductible. We will eat it.”

It sounds like a great deal.

In reality, it can put you in the middle of insurance fraud.

Important note: This article is educational and not legal advice. If you have questions about your specific policy or claim, talk with your insurer or an attorney.

Why your deductible matters (and why it is not optional)

Your deductible is the portion of a covered loss you agreed to pay under your insurance policy.

It is the “skin in the game” that helps prevent inflated claims and keeps premiums from spiraling even higher.

How the “we pay your deductible” scam usually works

A contractor cannot legally make your deductible disappear without moving money around somewhere.

In many cases, the only way to “waive” it is to submit paperwork that does not match reality.

The common playbook

- The roofer tells you they will cover the deductible.

- The roofer inflates the invoice or submits a false line item to the insurer.

- The insurer pays based on that inflated number.

That is not a discount. That is misrepresentation.

The risk is not just on the contractor

Insurers are cracking down in 2026. Claims get audited. Documentation gets reviewed.

If an audit finds inflated invoices or false statements, the homeowner can be pulled into the investigation because the claim was submitted under the homeowner’s policy.

Even if you did not “intend” fraud, signing documents you did not understand or accepting a kickback-style arrangement can create serious headaches.

The quality trap: how they “find” the money

Ask yourself this:

If a roofer is willing to lie to a billion-dollar insurance company, do you think they are telling you the truth about your roof?

To “eat” a $1,000 to $2,000 deductible and still make a profit, the contractor has to recover that money somewhere.

Common corner-cutting we see:

- Using cheaper underlayment instead of proper ice and water protection where it matters

- Reusing old vents or flashing instead of replacing worn components

- Rushing labor or using unqualified crews

- Skipping ventilation details that protect the roof long-term

The roof might look fine on day one. The problems show up later.

What to do if a roofer offers to pay your deductible

Use this quick checklist.

Ask directly

- “Will I be paying my deductible out of pocket?”

- “Will the invoice to the insurance company match the actual contract price?”

- “Can you put your deductible offer in writing?”

If they refuse to answer clearly, that is your answer.

Get a second opinion

A reputable storm damage contractor should be comfortable with:

- Transparent pricing

- Clear scope of work

- Proper documentation

- No “creative” billing

The Mighty Dog approach: do it legally and sleep well at night

At Mighty Dog Roofing of Rhode Island, we do not commit fraud.

We help homeowners by:

- Documenting storm damage properly

- Supporting the claim process with clear scope and photos

- Offering financing options to help cover deductible costs legally

You should not have to choose between a quality roof and a clean record.

If you are in Cranston or Western Cranston (02921) and you need a storm damage roof assessment, we can help you document the damage and navigate the process the right way.

Call (401) 425-4108 or visit our Contact Us page.

Rhode Island Service Locations:

Ashaway, Barrington, Bradford, Bristol, Carolina, Central Falls, Charlestown, Chepachet, Clayville, Coventry, Cranston, Cumberland, East Greenwich, East Providence, Exeter, Forestdale, Foster, Glendale, Greene, Greenville, Harrisville,Hope,Hope Valley, Hopkinton, Jamestown, Johnston, Kenyon, Kingston, Lincoln, Little Compton, Manville, Mapleville, Middletown, Narragansett, Newport, North Kingstown, North Providence, North Scituate, North Smithfield, Oakland, Pascoag, Pawtucket, Portsmouth, Providence, Riverside, Rockville, Rumford, Saunderstown, Shannock, Scituate, Slatersville, Smithfield, Tiverton, Wakefield, Warren, Warwick, West Greenwich, West Kingston, West Warwick, Westerly, Wood River Junction, Woonsocket, Wyoming

FAQ

Is it illegal for a roofer to pay my deductible in Rhode Island?

It can be. Many “waive the deductible” offers rely on inflated or false invoices submitted to the insurer, which can be considered insurance fraud.

Can a contractor reimburse my deductible in Cranston?

In general, schemes to reimburse, rebate, or “absorb” the deductible can function like a kickback and may violate insurance rules. If you are unsure, confirm with your insurer.

What is a safer way to handle my deductible after storm damage?

Work with a reputable local contractor who documents the damage, provides transparent pricing, and offers legal options like financing if you need help managing out-of-pocket costs.